Key findings

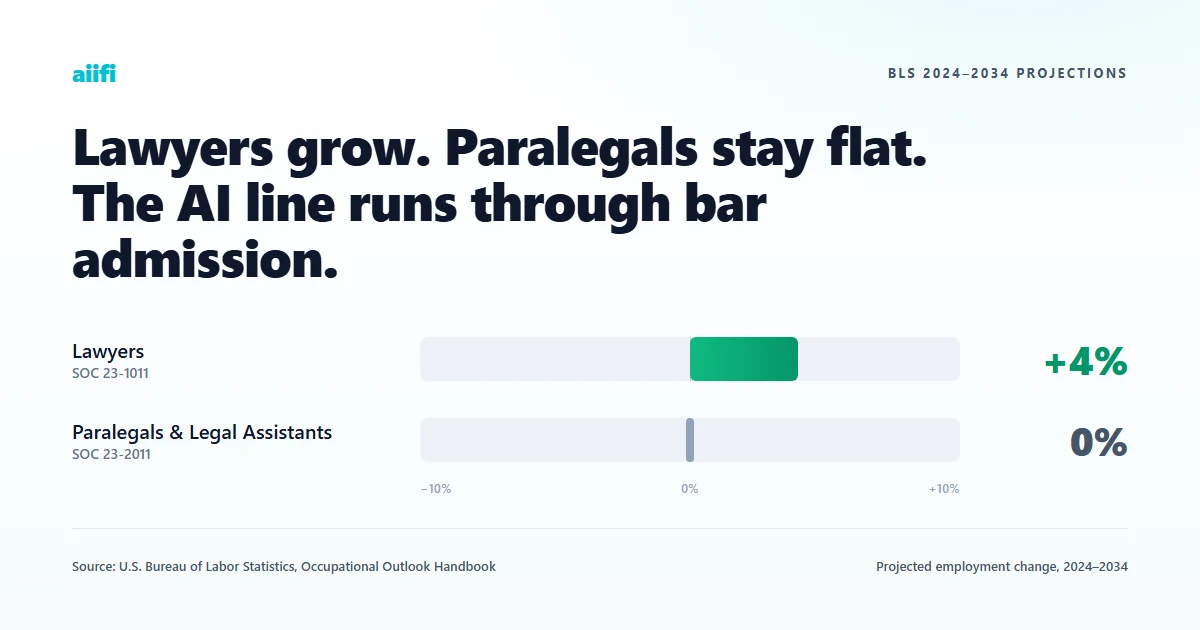

1. Accountants and bookkeepers track opposite directions.

BLS projects accountants and auditors to grow 5% through 2034 while bookkeeping clerks decline 6%. The two roles are often grouped together but face opposite AI outlooks.

2. BLS itself names software automation as the cause.

The BLS Occupational Outlook Handbook states that "software innovations have automated many of the tasks" performed by bookkeeping clerks. The automation narrative is documented in primary labor-market data, not just industry opinion.

3. GenAI adoption in professional services has nearly doubled in a year.

Organizational adoption rose from 22% to 40% between the 2025 and 2026 Thomson Reuters surveys. This is current state at a material share of firms, not future state.

4. AI is already widely used for tax research.

Thomson Reuters' 2026 AI in Professional Services Report found 69% adoption among tax and accounting professionals. Routine analytical work is no longer fully human-driven.

5. AI fluency commands a measurable wage premium.

PwC's Global AI Jobs Barometer 2025, based on nearly a billion job ads, found AI-skilled workers in business and finance roles earn a 56% wage premium. AI fluency translates into measurable career value.

Why Is This Question More Complicated Than It Looks?

The phrase "accountants" blurs two occupations the BLS tracks separately. Accountants and Auditors (1,579,800 jobs in 2024) and Bookkeeping, Accounting, and Auditing Clerks (1,613,400 jobs) are almost the same size, but their AI outlooks are opposite. Most articles on this topic conflate them and draw the wrong conclusion about accounting careers.

| Accountants & Auditors | Bookkeeping, Accounting, and Auditing Clerks | |

|---|---|---|

| 2024 jobs | 1,579,800 | 1,613,400 |

| 2024–2034 outlook | +5% growth | −6% decline |

| Annual openings | ~124,200 | ~170,000 (mostly replacement) |

| Median pay (2024) | $81,680 | $49,210 |

BLS is unusually direct about the cause of the clerk decline. Its own Occupational Outlook Handbook says "software innovations have automated many of the tasks" performed by bookkeeping, accounting, and auditing clerks. For accountants and auditors, the same publication predicts that routine-task automation "will make their advisory and analytical duties more prominent" rather than reducing total demand.

The 170,000 annual openings BLS projects for clerks is easy to misread as growth. It is not. BLS explicitly flags most of these openings as replacement, meaning backfills for retirements and people leaving the occupation for other work, inside a pool that is shrinking by 6% over the decade. The openings number tells you how many doors will open. The outlook number tells you the pool behind the doors is contracting.

What actually differentiates AI exposure inside accounting is task mix, not job title. An entry-level accountant who spends most of their week on month-end journal entries and bank reconciliation has more in common with a bookkeeping clerk's AI exposure than with a controller's. The role distinction matters, but the task distinction matters more, which is what the next section answers.

Which Accounting Tasks Can AI Automate Today?

The tasks AI can handle end-to-end today include transaction coding, bank reconciliation, and document summarization. Thomson Reuters' 2026 AI in Professional Services Report, based on a survey of 1,514 professionals, found document summarization at 57% adoption and document review at 55% among current GenAI users in tax and accounting. Tasks requiring judgment, sign-off, or client context still need a human, but AI is now assisting many of them.

| Task | AI capability today | Human still needed for | Risk level |

|---|---|---|---|

| Transaction coding | High | Edge cases, judgment calls | High |

| Bank reconciliation | High | Exception handling | High |

| Document summarization | High | Interpretation, context | High |

| Document review | High | Final sign-off | Medium |

| Standard tax return preparation | Moderate | Complex cases, review | Medium |

| Tax research | High | Application, client advice | Medium |

| Audit procedures | Moderate | Judgment, controls opinion | Low |

| Financial analysis and advisory | Low | All of it | Low |

Risk level reflects (a) whether AI can currently perform the task end-to-end, (b) current adoption evidence from industry reports, and (c) whether human sign-off is legally or ethically required. It is not a timeline prediction.

The highest-risk tasks all share a structure: high volume, rules-based, structured input, and a standard output format. Bank reconciliation is the clearest example of how the work changes. Old workflow: a bookkeeper pulls the bank statement, opens the general ledger, matches each transaction line by line, investigates discrepancies, and adjusts entries until the two sides reconcile. AI workflow: the system ingests both feeds, matches the overwhelming majority of transactions automatically, and flags a small set of exceptions for human review. The human's time shifts from line-by-line matching to exception handling and sign-off. Transaction coding follows the same pattern: a bookkeeper who used to code 400 transactions a day now reviews AI-coded entries and intervenes on the outliers.

Tax research is interesting because it is high adoption but medium risk. ACCA's January 2026 PCRT guidance on AI in tax work confirms that AI is already being used for tax compliance data collation, report drafting, due diligence, research, and high-volume return processing. The reason it stays medium risk rather than high is that applying tax research to a specific client situation, defending a position, and taking responsibility for the advice still require a human professional. AI is doing the retrieval; the accountant is doing the judgment.

Audit procedures sit at the safer end for a different reason. CPA.com's 2025 AI in Accounting Report notes that audit innovation is more methodical than other accounting disciplines because of regulatory and liability complexity. AI can analyze controls, flag anomalies, and accelerate testing, but the professional sign-off on an audit opinion carries legal weight that firms will not delegate to a model in the near term.

How Are Accounting Firms Actually Using AI in 2026?

The era of early AI adoption in professional services has passed. Thomson Reuters' 2026 report describes 2026 as the strategic phase of AI, with organizational adoption doubling year-over-year from 22% to 40%. Among active users, 82% use GenAI at least weekly. For accountants, the question has shifted from whether AI will be used in their firm to how well it will be used.

- Adoption has reached a tipping point. GenAI organizational adoption nearly doubled in twelve months (Thomson Reuters 2026). Only 19% of firms have no plans to adopt. Firms that weren't using AI a year ago have adopted it since.

- Usage is no longer experimental. 82% of current GenAI users use it at least weekly (TR 2026). Once a firm crosses the line, the tools become embedded in workflow rather than sitting as optional add-ons.

- Performance gaps are opening between adopters. PwC's 2026 AI Performance Study, covering 1,217 senior executives across 25 sectors, found that 20% of firms are capturing 74% of AI's economic value, and leaders generate 7.2x more revenue and efficiency gains than the average firm. The pattern is cross-industry, but accounting is one of the 25 sectors, and the same leaders-versus-laggards split is visible in professional services per Thomson Reuters' adoption data. AI impact is uneven by firm, not just by role. The question is no longer whether AI is working, but which firms are capturing the most value from it.

- The next wave is agentic. 15% of firms use agentic AI today; 53% are planning or considering it (TR 2026). The shift from "AI that answers questions" to "AI that takes actions inside a workflow" is the near-term structural change.

- Adoption is outpacing measurement. Only 18% of professional-services firms track AI ROI (TR 2026). Firms are implementing first and justifying second, which is the signature of fast-moving disruption.

Adoption is not uniform, and the reasons are specific. The overall average hides wide variation by discipline: firms deploying AI on tax research and document work move fast; firms deploying AI into audit workflows move slowly. Regulatory and liability concerns are the binding constraint in audit (CPA.com 2025), and ACCA's January 2026 PCRT guidance adds a firm-wide layer, stating that members remain responsible for any work produced regardless of AI involvement. Professional accountability is where adoption slows, not capability.

This pace of change means the question "could AI do my job?" is no longer the right one. The more useful question is: which parts of your job are already being done by AI at firms like yours, and which parts are not? That is what the next two sections answer.

Which Accounting Roles Are Most Exposed to AI?

The most-exposed accounting roles are built on repetitive, rules-based, high-volume processing. Bookkeepers, AP/AR clerks, routine tax-return preparers, and junior month-end staff face the most pressure. BLS projects a 6% decline for clerks through 2034, and Thomson Reuters shows current firm adoption targeting exactly their task mix.

Bookkeeping clerks face the most direct pressure. Their core tasks (transaction coding, bank reconciliation, recording financial data in accounting software) are all classified as high-risk in the task table above. This is the only accounting-family occupation for which BLS itself names software automation as the driver of projected decline.

Transaction coding and bank reconciliation are both high-risk in the task table, and AP/AR clerical roles are built almost entirely on these two activities. These roles are less clearly tracked by BLS than "bookkeeping clerks" as a category, but their task mix overlaps heavily with clerks, and CPA.com's 2025 report notes that AI is automating routine work traditionally assigned to entry-level finance staff. The risk here is task-driven rather than role-title-driven.

For routine tax-return preparers working in high-volume, low-complexity environments, the pressure comes from two directions. Tax research at 69% adoption (Thomson Reuters 2026) and standard return prep being automated (ACCA January 2026 guidance) both cut into the work that has traditionally justified junior tax staff. Complex advisory tax work is a different story and appears in the next section; it is specifically routine, repeatable return work that is most exposed.

Entry-level staff doing repetitive month-end work sit in a similar position. CPA.com's 2025 report is explicit: AI is automating routine work traditionally assigned to entry-level accounting hires. The task-automation table above shows why. A junior accountant whose week is 70% journal entries, reconciliations, and document review is working almost entirely in the high-risk quadrant: all three of those task categories are classified high-risk in the table above. This does not mean entry-level hiring disappears, but the job description shifts, and the next section explains what it shifts toward.

Which Accounting Roles Are Safer From AI?

The safer accounting roles are built on judgment, exception-handling, regulation, and client relationships. Auditors doing substantive review, complex tax advisors, controllers, and advisory-focused CPAs are projected to grow. BLS's +5% outlook for accountants and auditors is driven by exactly this advisory shift, and Thomson Reuters confirms AI is assisting these roles, not replacing them.

Judgment-heavy auditors sit in the safest position. Audit procedures are low-risk in the task table because regulatory and liability complexity keep human professionals as the responsible party. CPA.com's 2025 report states that audit innovation is more methodical for this reason and that new tools are helping firms focus on higher-concept work requiring professional judgment. The specific capability gap is evidence evaluation and sign-off: AI can produce a draft memo or surface an anomaly, but it cannot take legal responsibility for the audit opinion. That responsibility stays with the human.

Complex tax advisors are protected by the gap between retrieval and application. Tax research has high adoption, but the task is medium-risk because applying research to a specific client situation requires professional reasoning, accountability, and client trust. Thomson Reuters' 2026 report is explicit that AI "is not a substitute for human reasoning" and that human oversight remains necessary. AI retrieves and drafts; the human weighs the client's risk tolerance, the regulator's likely interpretation, and the strategic tradeoff between available positions. Those weightings cannot be generated from retrieval alone. For advisors handling non-standard situations, that weighting is the job.

Controllers and finance managers benefit from a broadening mandate rather than a contracting one. BLS's advisory-shift language ("advisory and analytical duties more prominent") maps cleanly onto this role. Financial analysis and advisory are low-risk in the task table. The day-to-day shifts from producing the analysis to interpreting AI-assisted analysis, challenging it, and translating it into operational decisions. What AI cannot do is negotiate with operational teams, defend an interpretation in an executive forum, or absorb accountability for a number the board acts on.

Client-facing advisory CPAs are the clearest growth path. This is the direction BLS implicitly describes when it says accountant demand will not fall but advisory duties will become more prominent, and it is the direction PwC's wage data points to as well. PwC's Global AI Jobs Barometer 2025 found that AI-skilled workers command a 56% wage premium in business and finance roles. The capability gap AI cannot close here is relationship context: reading tone in a meeting, understanding what a CFO does not say, adapting a recommendation to a client's evolving strategic priorities. Accountants who move toward advisory and develop AI fluency are in the compounding tier.

How Should Accountants Learn AI?

The skills accountants should build now are the ones that pair with the high-risk tasks AI is already doing. Three themes cover most of the shift: AI output validation, exception handling, and advisory interpretation. Learning these does not require coding. It requires structured practice reviewing AI work, and it maps directly to the tasks in the table above.

AI output validation. Document review (high-risk, 55% current adoption per Thomson Reuters 2026), transaction coding, and document summarization are increasingly AI-assisted. The skill shift across all three is from performing these tasks to catching errors, hallucinations, and context misreads in AI output. Accountants who can review AI work quickly and confidently will be more valuable than those who either do the work manually or trust AI outputs blindly.

What this looks like in practice: a bookkeeper runs AI over 200 transactions, accepts 185 as correctly coded, flags 8 for manual recoding based on unusual vendor patterns, and feeds the 7 outright AI errors back to the firm's AI lead. The human's value is not the coding. It is the triage speed and the pattern-recognition feedback loop.

Exception handling. Bank reconciliation, standard journal entries, and standard tax return preparation are the most structured clerical work in accounting. The shift is from processing every entry to triaging AI-prepared entries, catching the ones AI misreads, and documenting the exception patterns back to the team. Exception handling is not a new skill in accounting, but the job description is inverting: it used to be the exception; now it is the work.

What this looks like in practice: a junior accountant running a month-end close used to post 400 entries manually. Now AI drafts 380 of them. The accountant's work is the remaining 20 edge cases (foreign currency, intercompany, accrual judgment) and a review pass over the 380 to catch the 2 or 3 that AI got wrong. Output tripled and the skill mix changed.

Advisory interpretation and client communication. The low-risk tasks in the table (financial analysis, advisory, audit judgment) are where AI now generates first-pass work. The accountant's value becomes interpreting that work in context, explaining it to clients, and challenging it where the model missed something specific to the situation. This is the skill that maps to the wage premium PwC measured.

What this looks like in practice: a controller preparing a monthly board pack used to spend 4 hours running variance analysis across 30 budget lines. Now AI drafts the analysis in 20 minutes. The controller spends the saved time stress-testing the top 5 variances ("does this growth really hold if we exclude the one-off inventory write-down?"), pre-empting the questions the CFO always asks, and preparing a clear recommendation the board can act on. The deliverable shifted from reconciled numbers to an explained decision.

What Are the Best AI Courses for Accountants?

The best AI courses for accountants teach practical AI use without requiring coding and pair directly with the validation, exception handling, and interpretation skills above. Three options cover most of the learning path for a non-technical professional.

-

Best for: practical AI fluency without coding.

A short, accessible introduction that covers prompting, verification, and everyday AI use. See the full review for current pricing and enrollment data.

-

Prompt Engineering for ChatGPT (Vanderbilt)

Best for: structured prompting skills that apply across document work, review, and analysis.

University-taught, highly rated, and one of the most direct fits for the AI output validation skill described above.

-

Best for: accountants who want to take several AI and data-analysis courses under one subscription.

The break-even math and full comparison are in the linked guide.

How We Researched This

This analysis synthesizes 11 primary sources across three categories:

- Government data (5): BLS OOH for Accountants and Auditors, BLS OOH for Bookkeeping Clerks, O*NET 13-2011.00, O*NET 43-3031.00, O*NET 13-2082.00 for Tax Preparers.

- Industry reports (5): Thomson Reuters 2026 AI in Professional Services Report, CPA.com 2025 AI in Accounting Report, PwC Global AI Jobs Barometer 2025, PwC 2026 AI Performance Study, ACCA January 2026 PCRT guidance.

- Peer-reviewed academic (1): Eloundou et al., Science, 2024.

Author. The Aiifi Team synthesized this analysis in April 2026 from primary labor-market data (BLS, O*NET) and current industry reports (Thomson Reuters, CPA.com, PwC, ACCA). The Aiifi Team is positioned as AI and online learning analysts, not practising accountants. Every role classification in this article is supported by at least one task-level signal from O*NET or Thomson Reuters plus at least one additional labor-market or adoption signal.

Classifications used in this article:

- Most exposed: repetitive, rules-based, structured-input work with current adoption evidence and, where applicable, a BLS-projected decline.

- Safer: exception-heavy, regulated, judgment-heavy, or client-facing work where professional sign-off is required or where BLS projects growth.

- Risk level (task table): whether AI can perform the task end-to-end, current adoption evidence, and whether human sign-off is legally or ethically required. Not a timeline prediction.

What this analysis did not do:

- No original survey research.

- No licensed job-posting data (Lightcast or equivalent).

- No proprietary labor-market analytics.

- Salary and wage-premium figures are from published third-party studies.

Editorial independence. This page is editorially independent. Course recommendations are not paid or sponsored, though internal links point to affiliated course guides where relevant.

Freshness. Reviewed April 2026. Updated when BLS OOH refreshes, when a new Thomson Reuters, CPA.com, or PwC AI report is published, or when significant new labor-market data emerges.

Frequently Asked Questions

Will AI replace bookkeepers before accountants?

Yes. BLS projects bookkeeping, accounting, and auditing clerks to decline 6% through 2034 while accountants and auditors grow 5%. BLS explicitly names software automation as the reason for the clerk decline. The split is driven by task mix, not job title, which is why some accountants with clerk-heavy workloads face similar pressure.

How long before AI replaces accountants?

No defensible public timeline exists. BLS projects outlook through 2034 without naming an end state, and industry reports track adoption curves rather than displacement timing. Any specific year ("accountants gone by 2030") is speculation, not data. The more answerable question is how fast tasks are being automated, which is current state, not future state.

Is accounting still a good career in 2026?

Yes, for accountants moving toward judgment-heavy, advisory, or audit work. BLS projects 5% growth for accountants and auditors through 2034, and PwC's Global AI Jobs Barometer 2025 found AI-skilled workers command a 56% wage premium in business and finance roles. The career risk is concentrated in repetitive clerical work, not in the profession as a whole.

Will AI replace tax accountants?

Partially. Thomson Reuters' 2026 report shows tax research at 69% adoption and document summarization at 57%, meaning AI is already handling retrieval-heavy tax work. Standard high-volume return preparation faces pressure. Complex tax advisory, where applying research to a specific client situation requires professional accountability, remains safer.

Will AI replace auditors?

Not in the near term. CPA.com's 2025 AI in Accounting Report notes audit innovation is more methodical than other accounting disciplines because of regulatory and liability complexity. AI assists audit work (analyzing controls, flagging anomalies, accelerating testing), but professional sign-off on an audit opinion carries legal weight that firms will not delegate.

What AI skills do accountants need in 2026?

Three: AI output validation (reviewing AI-generated work for errors and context misreads), exception handling (triaging AI-prepared entries and documenting patterns), and advisory interpretation (explaining AI-assisted analysis to clients and challenging it). None require coding. See the skills section above for what each looks like in practice.

Are AI certifications worth it for accountants?

Yes, when chosen well. Short, practical AI courses aligned with the skills above (output validation, prompting, AI-assisted workflow) are more useful than broad AI overviews or coding-heavy programs. The AI course guides on this site review specific options with current pricing and fit analysis.

Sources

Government and labor-market data

- U.S. Bureau of Labor Statistics. "Occupational Outlook Handbook: Accountants and Auditors." Last modified August 28, 2025. https://www.bls.gov/ooh/business-and-financial/accountants-and-auditors.htm

- U.S. Bureau of Labor Statistics. "Occupational Outlook Handbook: Bookkeeping, Accounting, and Auditing Clerks." Last modified August 28, 2025. https://www.bls.gov/ooh/office-and-administrative-support/bookkeeping-accounting-and-auditing-clerks.htm

- O*NET OnLine. "13-2011.00 Accountants and Auditors." Updated 2026. https://www.onetonline.org/link/summary/13-2011.00

- O*NET OnLine. "43-3031.00 Bookkeeping, Accounting, and Auditing Clerks." Updated 2026. https://www.onetonline.org/link/summary/43-3031.00

- O*NET OnLine. "13-2082.00 Tax Preparers." Updated 2026. https://www.onetonline.org/link/summary/13-2082.00

Industry reports

- Thomson Reuters Institute. "2026 AI in Professional Services Report." February 2026. https://insight.thomsonreuters.com.au/legal/resources/resource/2026-ai-in-professional-services-report

- CPA.com. "2025 AI in Accounting Report." June 10, 2025. https://www.cpa.com/news/cpacom-issues-2025-ai-accounting-report

- PwC. "Global AI Jobs Barometer 2025" (labor market and wage effects). https://www.pwc.com/gx/en/issues/artificial-intelligence/ai-jobs-barometer.html

- PwC. "2026 AI Performance Study" (firm performance and ROI effects). April 13, 2026. https://www.pwc.com/gx/en/news-room/press-releases/2026/pwc-2026-ai-performance-study.html

- ACCA. "Ethical Use of AI in Tax Work (PCRT Topical Guidance)." January 19, 2026. https://www.accaglobal.com/content/dam/ACCA_Global/Technical/PCRT/PCRT-AI-guidance-0126.pdf

Academic

- Eloundou, T., Manning, S., Mishkin, P., & Rock, D. (2024). "GPTs are GPTs: Labor Market Impact Potential of LLMs." Science 384(6702): 1306–1308. https://www.science.org/doi/10.1126/science.adj0998

What to Read Next

If these findings make you want to build AI skills, see the AI course guides, starting with Google AI Essentials for non-coders. For broader perspectives on AI and work, 24 expert quotes on AI and jobs. By Aiifi Staff. This article was last reviewed in April 2026.